Hey Fintech Friends! In this edition of our FinWise newsletter, we’re excited to share a variety of top hits ranging from recent announcements, product news, to insights from your favorite industry experts. Ready to Fly with FinWise? 🦉

News recap.

- Latest Podcast(s)

- Phil Goldfeder from American Fintech Council, Navigating the Fintech Regulatory Landscape

- David Shipper from Datos Insights, Card Trends Unveiled

- Alex Johnson, Creator of Fintech Takes, Decodes Financial Nihilism, AI and the Future of Banking

- Latest Update(s)

Product spotlight.

1. Credit Enhancement. What is it, and how does it benefit FinWise Bank’s strategic partners?

Addresses the challenges that lending and card programs face securing warehouse facilities and managing capital requirements.

2. The Landscape of Real Time Payments on MoneyRails™

FinWise has deployed its MoneyRails™ payments hub solution, a modern payments hub system. The Bank’s MoneyRails™ solution will allow Fintechs and other businesses to safeguard deposits and process large numbers of payments via API.

As part of the MoneyRails™ buildout, the Bank wanted to make sure we could send money instantly to most US bank accounts. As the world is becoming increasingly fast, customers’ expectations are changing as well. When all is at your fingertips, it is only fair to expect money to move at the speed of light.

Prior to the introduction of real time payments (RTP) in 2017, Banks had two ways of sending money in (near) real time:

- Wires

- Push to Cards

While wires were widely adopted as one of the most ancient payment rails, being able to send money through a push to card transaction was offered by a very limited number of Financial Institutions (even though most Banks can receive a push to card transaction).

The landscape has since evolved with the introduction of The Clearing House’s Real Time Payments (RTP), and the Federal Reserve’s FedNow solutions.

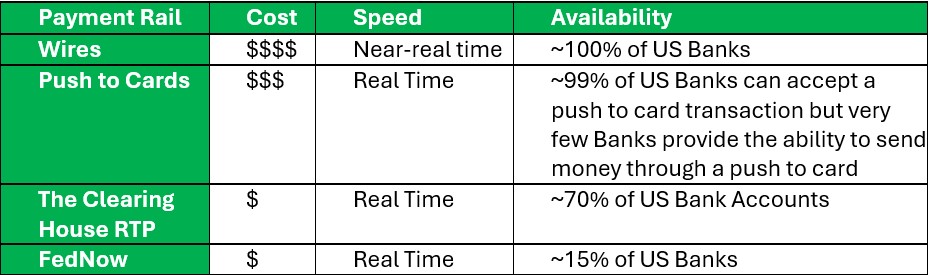

Let’s take a look at how all these rails compare:

These rails vary quite tremendously in terms of pricing and availability, but not in speed. MoneyRails™ supports every single one of these rails. As such, FinWise gives complete freedom to its users to decide whether to maximize availability at a higher cost or minimize cost and still be able to reach a high level of coverage. It all depends on the use case!

While these newer rails have proven to be competitors for the legacy ACH service, ACH still has the upper hand on being able to pull money from an account.

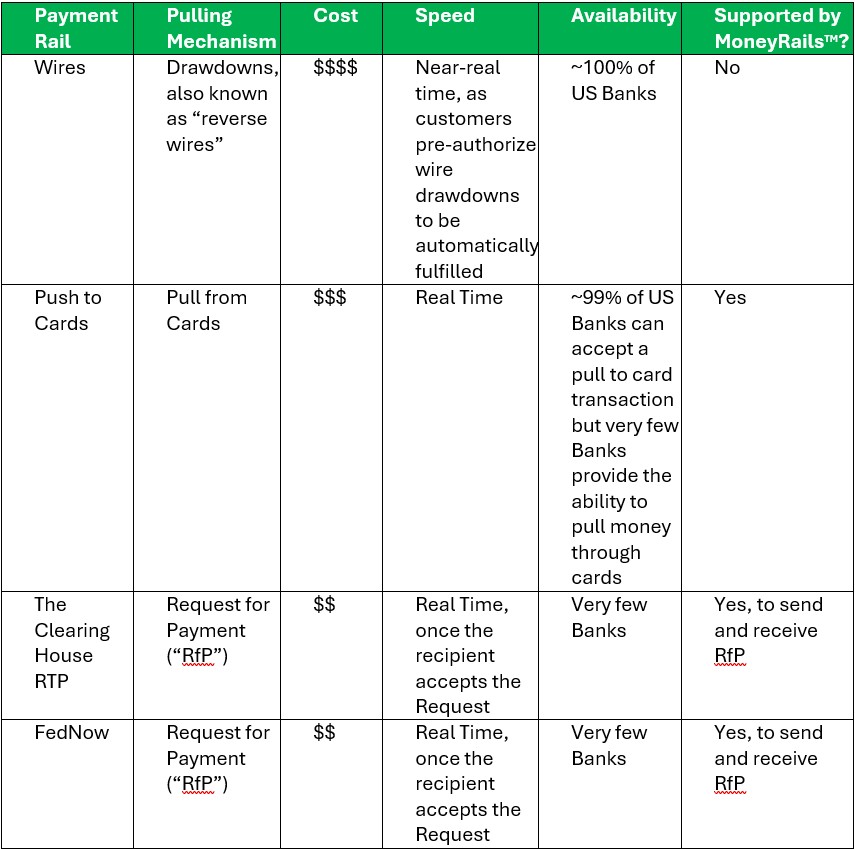

Let’s take a look at how these rails compare to ACH for funding transactions:

The Clearing House and FedNow have made the design decision not to allow for a mechanism that is similar to ACH Debits. There is currently no way to pre-authorize pull transactions to be done via RTP and FedNow, limiting the use cases for both payment rails. Effectively, if a MoneyRails™ user wanted to pull money from an external account and that external account could support a Request for Payment, the process would go as follows:

- MoneyRails™ User sends a Request for Payment via API

- MoneyRails™ submits the request to TCH/Fed Reserve

- TCH/Fed Reserve forwards the request to the external financial institution

- The external FI prompts their use to accept or decline the request for Payment

- If accepted, the external FI fulfills the request for payment and funds are sent in Real Time

As you can see, the speed of transaction depends on how fast a recipient will fulfill the request. Effectively, this works a bit like when a user requests a payment from their Venmo or Zelle friends.

Additionally, FedNow and TCH have seen very little adoption from US Banks to implement their Request for Payment feature. Nonetheless, we believe there is a future for RTP and FedNow to make a splash and compete with ACH debits. As such, FinWise is one of the very few financial institutions to offer Request for Payment for both RTP and FedNow.

In the meantime, MoneyRails™ also supports “Pull from Cards”, which works a bit like using a debit card at a Point of Sale, except that once a transaction is approved, the funds are made available in real-time to the initiator of the transaction.

Thought leadership.

Guest Contributor:

Guest Contributor:

Nathan Lemon, IC Group

Trends to Get Your Card Top of Wallet

The credit and debit card industry is constantly evolving, driven by technological advancements, changing consumer preferences, and regulatory standards. These changes are reflected in the manufacturing processes and materials used to create secure cards.

In today’s competitive market, making your card stand out is more important than ever. Here are some of the latest advancements in card production and effective strategies to ensure your card stands out in a crowded wallet.

Potential Premium Printing Techniques for Cards

- Color Core: This simple adjustment to the card build enables cardholders to easily identify your card in a crowded wallet. Custom colors, metallic inks and patterns are available in the market today.

- Metallic Foil Stamping: Applying metallic foil in silver, gold, or other colors creates a reflective, eye-catching effect that enhances the card’s visual appeal and gives the card a premium appearance.

- Laser Engraving: This precise technique etches designs or text into the card surface, creating a permanent and sophisticated finish.

- Spot UV Coating: Applying a high-gloss coating to specific areas of the card creates contrast and highlights design elements, adding a touch of depth and dimension. When paired with a matte finished base design, a financial institution logo or fintech brand can stand out with this subtle embellishment.

- Less Is More: Fintech companies have successfully reduced the amount of information on the card to highlight their branding with a more modern look and feel.

Card Design Matters.

Recent surveys indicate over 80% of younger consumers (Millennials and Gen Z) consider the design of their payment cards an important factor in their usage decisions (1).

Not only does personalization and customization create unique differentiation that drive consumer engagement, but more importantly for issuers, this increased engagement results in higher usage, higher spend, and ultimately increased interchange revenue.

While metal cards are the benchmark today for premium offerings, innovations in inlay technology and materials are redefining ways to deliver a “premium” card.

Novoflex shared with us some of their cutting-edge technology for creating unique card designs and materials. They have a proprietary laminate solution that creates custom shaped EMV chips, while improving security and reducing carbon footprint.

FinWise Insights.

Sarah Grotta,

Sarah Grotta,

Deputy Fintech Officer at FinWise Bank

The Whirlwind in Washington

Tracking Regulatory and Legislative Changes Impacting Cards, Payments, and Fintech

The financial services industry is in a state of flux as the new administration rolls out significant policy shifts. Executive orders and new political appointees are reshaping regulatory priorities, while Congress considers bills that could dramatically alter credit card interest rates and payment card network structures.

For banks, fintech firms, and payment providers, understanding these changes is critical to staying compliant and competitive. I am tracking these changes and want to share them here, and as things are constantly changing will try to keep things updated for future editions.

Key Executive and Regulatory Changes

Temporary Order Halting New Regulations

One of the administration’s first moves was issuing an executive order pausing new regulations, impacting agencies such as the Consumer Financial Protection Bureau (CFPB) and Office of the Comptroller of the Currency (OCC).

📌 The Impact for Financial Services:

- This halts new rulemaking, including proposals in early stages, which many businesses see as temporary relief.

- However, recently enacted regulations still stand, subject to ongoing litigation in the courts, such as:

- Dodd-Frank Section 1033 – Consumer financial data rights.

- Dodd-Frank Section 1071 – Small business lending data collection requirements.

- Payday Lending Rule – Upcoming compliance date of March 30, 2025 still in effect as of this writing.

🔎 Key Takeaway:

While this provides short-term regulatory stability, banks and fintechs must still comply with existing laws and prepare for future shifts.

CFPB Directive to Halt New Investigations and Rulemaking

The administration has directed the CFPB to suspend proposed rules and enforcement actions, effectively reducing its regulatory influence in the near term.

📌 The Impact for Financial Services:

- The CFPB has dropped lawsuits against Capital One and Rocket Homes.

- Additional enforcement actions, such as those targeting Zelle P2P services, may also be reconsidered.

- While the agency cannot be dissolved without legislative action, this move signals a much lighter regulatory approach to financial services from the CFPB in new administration.

🔎 Key Takeaway:

- Short-term relief for financial institutions from the recent pace of new rules, but state regulators may fill the vacuum.

Executive Order Promoting Cryptocurrency and Digital Assets

The administration has reversed efforts to develop a central bank digital currency (CBDC) and instead supports market-driven crypto initiatives.

📌 The Impact for Financial Services:

- A light regulatory framework is being promoted to encourage private-sector digital asset innovation.

🔎 Key Takeaways:

- Increased institutional interest – Large financial firms may reconsider crypto offerings given the reduced regulatory risks.

- Regulatory uncertainty remains – While the government signals support, lack of formal guidance creates doubt.

Legislative Proposals Shaping Financial Services

10% Interest Rate Cap on Credit Cards

Senators Bernie Sanders (I-VT) and Josh Hawley (R-MO) have introduced a bill capping credit card interest rates at 10%, aiming to reduce consumer debt burdens. While this legislation has very little chance of becoming law, any bipartison support for federal interest rate limits must be taken seriously.

📌 The Impact for Financial Services:

- The current average credit card APR is 21.5% (Federal Reserve, 2024).

- A 10% cap would drastically alter credit card profitability and could force issuers to tighten lending criteria.

🔎 Key Takeaways:

- Lenders may adjust underwriting models to sustain profitability.

- Credit card rewards programs could shrink as issuers rebalance revenue streams.

New Requirement for Alternative Credit Card Payment Networks

A bill introduced by Senator Dick Durbin (D-IL) would require credit card issuers to offer merchants an alternative processing network beyond Visa and Mastercard.

📌 The Impact for Financial Services:

- Changes required to comply would likely cost fintechs, processors, and issuers billions as it did when the Durbin Amendment (2011), was implemented for debit cards.

🔎 Key Takeaways:

- Higher infrastructure cost and compliance fees associated with managing multiple network rules on a single card will result in fewer cardholder perks and more conservative underwriting models.

Key Appointments in Financial Regulation

The administration has made interim appointments and nominations to key financial regulatory positions, which will shape oversight and enforcement in the near term.

- Acting Director Consumer Financial Protection Bureau (CFPB) – Russell Vought Jonathan McKernan nominated for permanent position

- Nominated Commissioner of the Commodity Futures Trading Commission (CFTC) – Brian Quintenz

- Acting Chairman Federal Deposit Insurance Corporation (FDIC) – Travis Hill

- Acting Comptroller of the Currency (OCC) – Rodney Hood / Jonathan Gould nominated for permanent position

🔎 What This Means:

- New leadership = shifting enforcement priorities.

FDIC Withdrawal of Four Proposed Rules

On March 3, 2025, the Federal Deposit Insurance Corporation (FDIC) Board of Directors withdrew several outstanding proposed rules including those related to brokered deposits, corporate governance, and the Change in Bank Control Act (CBCA).

📌 The Impact for Financial Services:

- Brokered Deposits Restrictions: The proposed rule aimed to significantly revise regulations concerning brokered deposits, which could have disrupted various aspects of the deposit investment options.

- Corporate Governance and Risk Management: This proposal is intended to establish prescriptive standards for corporate governance and risk management for FDIC-supervised institutions with total consolidated assets of $10 billion or more.

- Change in Bank Control Act (CBCA): The proposal sought to amend filing requirements and processing procedures under the CBCA, potentially removing certain exemptions and requiring additional notices to the FDIC.

- Incentive-Based Compensation Arrangements: This proposed rule aimed to implement Section 956 of the Dodd-Frank Act, addressing incentive-based compensation arrangements that could encourage excessive risk-taking.

🔎 Key Takeaway:

- Regulatory Relief: The withdrawal of these proposals will reduce potential compliance burdens that banks and fintech firms would have faced had the rules been finalized.

- Strategic Reassessment: Financial institutions may want to reassess their governance and deposit strategies in light of the FDIC’s decisions.

- Future Rulemaking: The FDIC indicated that if it decides to pursue regulatory action on these matters in the future, it will do so by publishing new proposed rules or other issuances consistent with the Administrative Procedure Act.

Some thoughts on managing through all of this tumult

- While there’s a breather from new regulatory activity, the old ones still exist, and regulators will still expect compliance. Take the time that would have been dedicated to finding responses to new rules to create better approaches to dealing with the old.

- Pull a plan and policy together to determine if or how you will participate in the growth of digital currencies including stable coins.

- Consider new pricing models that could withstand new rules around fees and interest rates on financial services products.

- Pay more attention to state level legislatures and regulatory agencies that may want to fill the vacuum left by less active Federal agencies.

What’s Next?

We will continue tracking these developments and their impact on the financial industry. Stay tuned for updates in future newsletters.

📢 What regulatory changes are you most concerned about? Let us know!

Summary of Key Takeaways

✔️ Regulatory pause on new rulemaking, but existing rules still apply

✔️ CFPB scaling back enforcement, but state regulators may step up

✔️ Proposed interest cap could reshape lending and rewards programs

✔️ Alternative payment network legislation could increase costs for issuers

✔️ Financial institutions should reassess compliance, pricing, and advocacy strategies

Industry recognition as a Top-Performing Bank.

Connect with us.

Upcoming 2025 Events

- April 14-16, The Financial Brand Forum

- April 28-30, Alloy Labs Annual Member Meeting 2025

- April 28-30, NACHA Smarter Faster Payments

- May 7-9, Finovate Spring 2025

Join us on a FinWise Podcast found here:

|

|

|---|